The application process of getting a small business loan can be a daunting task. The questions start rolling in your head as a business owner: What business funding options are available to me? How do I qualify? What are the best rates for a small business loan? What documents do I need to get a business loan? What lenders do I work with to get a small business loan?

We all know it's not easy getting a loan from a bank. The common question is, "What do I do if I can’t get approved for a traditional bank loan?" Depending on the lender, getting a business loan is not easy. Bank loans are notorious for requesting copious amounts of paperwork and difficult qualifications.

At the end of the day, when you apply for a small business loan, it is not as challenging and overwhelming as you think. Still, small businesses do need to do some homework first and conduct the proper research of financing options when you apply for a business loan. So, here is how to apply for a small business loan.

5 Steps on How to Apply For a First-Time Small Business Loan

The following 5 steps to apply for a small business loan will guide small businesses through an orderly process in answering all of your questions and provide you a road map to discover what is available, how to prepare, apply, and determine which financing option is best for you. Read the following steps carefully.

Step 1: Why Do You Need to Apply for a Small Business Loan?

Small business owners searching for loans should always start with the question, Why? The need will definitely play a part in the decision when choosing a loan option. If it’s a large order of machinery or equipment or a business expansion that will require a lot of capital, a long-term solution will be necessary. If its cash flow or working capital needs, a shorter-term loan may be more suitable for that type of need. Determine the “why” and “how much” before taking additional steps.

Common "Why's" and business needs

- Working Capital (Cash Flow)

- Equipment

- Repairs

- Marketing

- Business Expansion

- Execute on Business Plan

- Real Estate Acquisition

- Recruitment

Step 2: What Are Your Qualifications/Credit Eligibility Requirements? How to qualify for a Business Loan.

6 common areas business lenders/funder’s review within the loan application in making underwriting and approval decisions include :

- Industry/Time in Business: The industry small businesses are in and the length of time of operation may dictate what loan products you will be eligible for.

- Credit Score Requirements: What kind of credit score do you need to get a business loan? The Personal credit score of the small business owner (s) involved plays a significant role in the decision-making process. The most common question about credit is “What credit score is needed for a loan?” Some loans require an excellent personal credit score from credit bureaus, while others expect good to fair credit scores. Bad credit is not an automatic disqualifier, in some cases, a small business owner can have bad or subprime personal credit, but options will be limited. The better your personal credit, the more loan options you can choose from. The business credit history and business credit score are derived in different ways. Business credit looks at how you pay your business debts, vendor credit, B2B transactions, and business taxes. Judgments, liens, and litigation can also play a role in an underwriting loan decision. We always suggest you monitor your credit bureaus and improve your personal and business credit history.

- Cash Flow: How you manage your small business cash flow places a vital role in your ability to acquire financing. Lenders will look at all business bank accounts from the last 3 to 6 months and evaluate a variety of factors in determining the small business’s ability to manage the cash flow of the business. The business bank operating account is evaluated for many factors that include:

- # of deposits per month

- Total monthly deposits

- Annual revenue

- What types of deposits and withdraws are being made

- Average daily balance

- Minimum daily balance

- Any late fees, overdrafts, and non-sufficient funds

4. Debt-To-Income Ratio: Lenders will look at the revenue versus any other business loans currently being made to see if the business can take on more debt.

5. Assets: Some business funding products will need to see cash reserves or physical assets like real estate, equipment, or other business assets to secure the financing.

6. Financial Statements: Long-term business loans and some business lines of credit, as well as larger loan amounts, will require the review of financial statements to determine eligibility. Common financial statements that may be reviewed include:

- Business income tax returns (sometimes personal tax returns as well)

- Year-to-date profit and loss

- Year-to-date balance sheet

- Accounts receivable ledger

- Accounts payable ledger

- Business plan

If you can improve your situation in any one of the above six areas, you may want to do some repairs before applying for any business loans to secure loan approval. You don’t need to give up your search if you have issues in any of the above categories if you need money now but understand that these factors will impact products, terms, and rates offered to secure loan approval.

Step 3: What Small Business Funding Options Are Available?

Here is a list of the 10 best small business lending options for small businesses.

Long-Term Loans, Business Loans

Long-term, small business loans are small business loans with a duration of over two years. Businesses are offered a fixed loan amount upfront and charged principal and interest. In this type of loan, unlike a line of credit, a business owner cannot draw money as you go with a long-term loan. Typically, long-term loans are for business expansion and growth or to finance large, long-term projects. This business funding loan product is used for long-term projects and needs at least $500,000 in annual revenue. This product is available from online lenders and many other types of originators.

Product Overview

Rates: Interest rates starting at 5.50% or treasury index plus 1% to 2.5%

Repayment: 2 to 10 years

Fees: Origination fees range from 0% to 3%

Payment: Monthly or bi-Weekly

Credit Profile: Good to excellent credit score preferred, all types considered

Loan Application: 1-page loan application, business bank account statements, financial statements

Business Line of Credit

A Business line of credit is an open, revolving line. This type of funding allows small business owners to draw funds when needed on-demand or make purchases—a line of credit charges a principal and interest rate. Business lines of credit have a credit limit that cannot be exceeded without approval. They are not open-ended forever and require renewal either semi-annually or annually to be extended. This business funding is primarily used for small purchases and working capital. No minimum annual revenue is needed to apply.

Product Overview

Rates: 5.50% Interest rates or treasury index plus 1% to 2.5%

Repayment: Open revolving line

Fees: Origination fees ranging from 0% to 3%

Payment: Monthly, bi-weekly or weekly

Credit Profile: Good to excellent credit score preferred, all types considered

Loan Application: 1-page loan application, financial statements

Small Business Credit Cards

Business credit cards are open, revolving credit lines that charge a principal and interest rate with a limit. Plastic credit cards are issued that can be used for making payments or purchases. Small business owners utilize business credit cards in conjunction with other financing products. The primary use of a business credit card is for the purchase of small items or working capital

Product Overview

Rates: Introductory rates start at 0% up to 28.99% principal & interest

Repayment: Open revolving line with a limit

Fees: $0 to $500 annual fees

Payment: Flexible monthly

Credit Profile: Must have good to excellent credit score and deep history

Short-Term Loans, Small Business Loans

Short-term business loans are typically repaid within 6 to 18 months. This type of loan features a lump sum offered up front with a fixed payback amount calculated using a factor rate over a short term of time. Rates are not principal and interest but cost more than traditional loans. Most businesses choose short-term small business loans when they do not qualify for traditional business funding.

Short-term small business loans charge more for costs and are shorter in time to repay. The payments are more frequent to compensate for the greater risks business lenders take in offering this product. Short-term small business loans are popular with small businesses because of the reduced documentation requirements and credit tolerances that are laxer than traditional small business loans. These short term loans are available from online lenders.

Product Overview

Rates: Factor rates range from 1.09% up to 1.45%

Repayment: 6 to 18 months in duration (typically 12 months or less)

Fees: 0% to 5% origination fees

Payments: Weekly, bi-weekly and in some cases daily

Credit Profile: All types of credit history considered

Loan Application: 1-page loan application, bank statements from a business bank account

Business Cash Advance

Business Cash Advances (BCA) are a Purchase of Future Sales Agreement. They advance future sales at a discount to a business. The business is responsible for paying back a fixed amount, which is greater than the amount that was advanced. This difference between the advance and payback amounts is called the “factor rate or cost.” This is not principal and interest costs. The advance is repaid by taking a fixed percentage of future overall deposits called the specified percentage. The payments are collected by an ACH fixed daily or weekly based on the specified percentage of future sales.

At the end of every month, reconciliation can occur. If the fixed payments taken are more than the set future percentage of sales, a business owner can request a refund back to the business for overpayment so that the set specified percentage of sales collected for the business matches the revenue volumes. Repayment continues until the amount is paid back in full. There is no term limit with advances as the fixed payback percentage changes due to fluctuating revenue. This small business financing product is available from online lenders as well as many other types of originators.

Product Overview

Rate: Factor rates range from 1.09% up to 1.45%

Repayment: No term limits. Payments continue until paid in full based on specified percentage collection method and are dependent on future revenues

Fees: Origination fees that range 0% to 5%

Payment: Weekly or daily

Credit Profile: All types of credit history considered

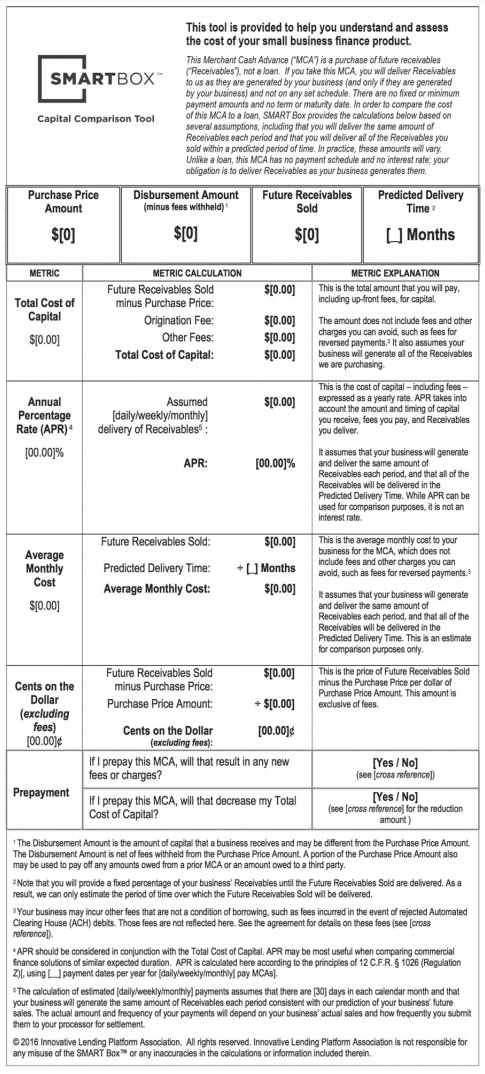

Merchant Cash Advances

A Merchant Cash Advance (MCA), also known as a Purchase of Future Sales Agreement, operates very similarly to BCA’s. The biggest difference is the repayment process, which is connected to future credit card revenues instead of overall sales. MCA’s take a set percentage of future credit card sales at the time of batch of credit cards until the advance is paid back in full. Business owners find this valuable when they have fluctuating revenues and don’t want to be locked into a fixed payment that could negatively impact capital or profit margins if revenues decline or fluctuate. This product is available from online lenders and many other types of originators.

Product Overview

Rate: Factor rates that range from 1.09% up to 1.45%

Repayment: No term limits (payoff depends on future credit card sales)

Fees: Origination fees range from 0% to 3%

Payment: Set percentage of future credit card revenues

Credit Profile: All types of credit history considered

Equipment Loans (Financing)

Businesses that use equipment to operate their business often turn to equipment financing to purchase equipment. You must have very good to excellent credit, but limited paperwork is necessary to get approved.

Product Overview

Rate: Factor rate ranging from 1.09% up to 1.45%

Repayment: 2 to 7 years

Fees: Origination fees range from 0% to 3%

Payment: Weekly or daily

Credit Profile: All types of credit history considered

Small Business Administration (SBA) Loans

The Small Business Administration (SBA) provides programs, guidelines, and loan guarantees to approved lenders for businesses. The Small Business Administration aims to help Americans successfully start, build, and grow their businesses. The SBA is not a lender and does not directly loan small businesses. The SBA provides a guarantee for SBA loans and allows the approved lender to take on the risk of business lending under SBA terms that they would not ordinarily do on their own. SBA loans are available from online lenders as well as many other types of originators.

Product Overview

Rate: Interest rates starting at 5.50%, treasury index plus 1% to 2.5%

Repayment Loan Terms: 3 to 25 years

Fees: Origination fees 0% to 3%

Payment: Fixed monthly

Credit Profile: Good to excellent credit scores are preferred, but all credit scores are considered.

Small Business Administration Loan Programs

SBA Standard 7 (a) loan program. SBA loan 7(a) is the SBA’s primary program and is designed to provide financial assistance to small businesses. The terms and conditions, like the guaranty percentage and loan amount, may vary by the type of loans and businesses.

SBA Loan Program 504. The SBA 504 loan is a powerful economic development loan program that will provide small businesses another avenue for business funding while promoting business growth and job creation. The use of proceeds from SBA 504 Loans must be used for fixed assets such as construction, commercial real estate, land or land improvements (and certain soft costs), or can also be used to refinance existing debt.

SBA Disaster Loans. Economic Injury Disaster Loans (EIDL) are a type of Small Business Administration loan that provides assistance after natural disasters like tornadoes, wildfires, or floods and when President Trump declared Covid-19 a nationwide emergency on March 13th, small businesses were able to access this program for emergency financing.

SBA Paycheck Protection Program (PPP) Loan (Coronavirus Relief Efforts). The Small Business Administration has established the Paycheck Protection Program loan. This SBA loan provides loans to small businesses affected by the COVID-19 crisis that need financial help. Second round of the Paycheck Protection Program is available through March 31, 2021.

Invoice Factoring

Invoice financing advances the outstanding balance to a business owner to increase the speed of cash flow to the business. This solution provides cash quickly and there is no need to wait for the client's outstanding invoices to be collected and received with invoice financing in place. Invoice financing has affordable costs ranging from 1% to 2.5% fee off of the face value of the invoice advanced. This product is available from online lenders as well as many other types of originators.

Product Overview

Rate: None

Repayment: No term limits

Fees: 1% to 3% fee based on the invoice. Monthly Service fees may apply depending on the volume of invoices factored.

Credit Profile: Credit scores of the clients need to be favorable NOT the business owner advancing off invoices.

Purchase Order Financing

Purchase order financing allows businesses to raise capital to pay suppliers upfront for verified purchase orders. Purchase order loans will finance an entire order or a portion of it, depending on the purchase order funder. When the supplier is ready to ship the order, the purchase order financing firm collects payment directly from the customer. The purchase order funder will subtract their fees and then send the balance of the invoice.

Product Overview

Rate: None

Repayment: No term limits

Fees: 1% to 3% fee for each purchase order. Monthly service fees depending on volume may also apply.

Credit Score: All parties need favorable credit history, but all credit scores considered

Step 4: Choosing Who To Work With when you Apply for a Small Business Loan:

Picking the best Business Loan Originator to help you with the loan application process is important.

The following is a list of the different types of business funding originators

- Traditional banks (Bank of America, Wells Fargo, Chase, etc.)

- Credit Unions

- Small Business Lenders

- Online Lenders (Fintech)

- Business Originating Marketplace’s

- Loan Broker’s

- Business Loan Officer

- Long-Term Business Lenders

- Equipment Financing Companies

- Invoice Factoring Companies

- Private Business Lenders

- Hard Money Business Lenders

- Commercial Real Estate Lenders

Every financial institution differs in what products and services they offer, so it’s important to ask what type of finance products they offer upfront to see if they can provide you the best options available in the marketplace.

How to Choose the Best Business Loan Originator

- Evaluate the expertise of the originator’s product knowledge

- Determine if they offer many financing options

- Ask how quick and efficient is the application process

- Check Reviews with third-party companies that don’t work directly with the business like the Better Business Bureau and Google. Trust Pilot is not reliable because they work directly with businesses and are compensated for their services.

- Make sure all offers come with disclosures or term sheets with all terms and conditions provided. Request a copy of the loan agreement before signing anything.

The 12 Warning Signs to Look Out for When Dealing With a Business Loan Originator

- Company Website. Check the broker or lenders website and look for whether the site looks current and informative. How does it stack up to other bank sites you use? Is there a section for legal information, privacy policy, location, and phone numbers for the various departments that can help you with more information or post-funding issues? With online lenders, you can trust them, but you need to verify that.

- Physical Address. Search the business address on google maps for a picture of the location. Check to see if it’s a true business address or if it’s a shared office space, co-work office, residential address, UPS Store, or mailbox center. Obviously, you would want to be working with a company that has an established business location.

- Company History. Check time in business with third-party sources like the Better Business Bureau. If the originator is less than 3 years of experience, you may want to ask for a resume of the person or company you are dealing with to see if they have good experience.

- No Independent Reviews. Check for independent reviews from Google or the Better Business Bureau to see how they handled the application process with other small businesses. Do not rely on companies like Trust Pilot, who work directly with business owners for a monthly service fee and have a controlled review business model. They do not have proper independence when considering customer reviews.

- Access/Communications. Does a live person always answer the phone? Is there a general number that you can talk to a customer service representative other than the person you are working with at the company? Always ask for direct numbers and the general company phone number. Check for service and response levels such as returning voicemails and email response times. If they take more than an hour to respond, that should raise warning flags

- Better Business Bureau. Is the business loan company a member of the BBB? Are they in good standing? Do they have any customer reviews?

- Any Federal, State, or Local Actions. Have they complied with all fair-lending laws? Are there any negative actions from federal, state, or local governments? Any customer lawsuits? Any employee lawsuits or actions?

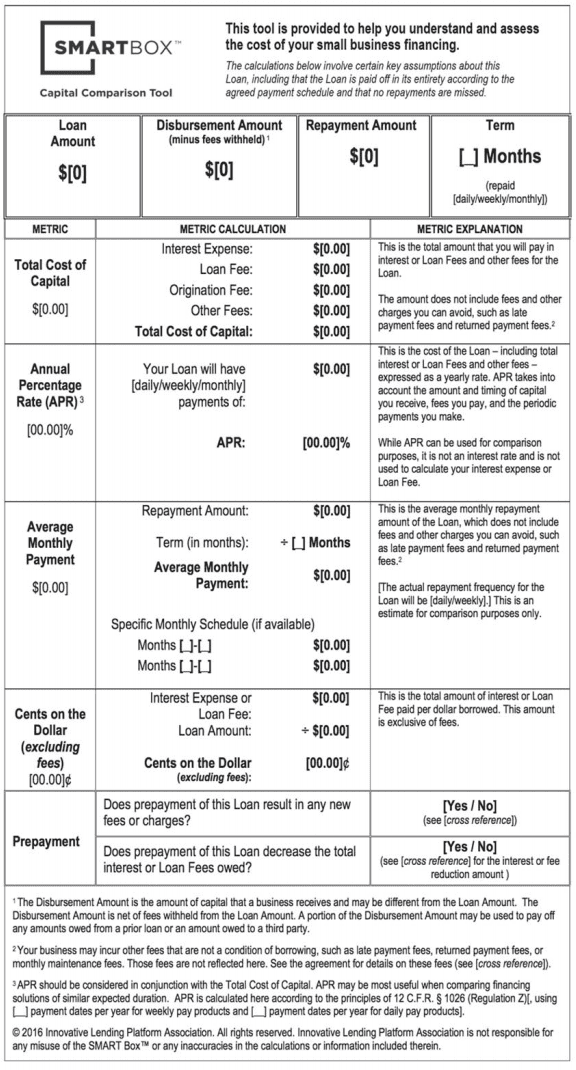

- No Clear Fee Disclosure or Term Sheet. All business loan originators should have disclosures such as a “Term Sheet” or “Smart Box Disclosure” that details all conditions, costs, and fees. Do not rely on offers that are in the body of an email like they were just giving you a general idea. The originator must have disclosures that can be emailed to you.

Samples of “Smart Box Disclosures”

- Credit Report Disclosure. Does the business loan originator offer a free copy of the credit report so you can see your personal credit they are evaluating? There are many business loan originators that will downplay your credit to convince you that you don’t deserve a better business funding product than the one they are offering. If the lender or broker provides a free credit report at the time of offer, this is a great sign that the company or broker is transparent and trustworthy.

- Time to Consider Offers and Quotes. Are they giving you enough time to consider the offer? Are they pushy and giving you an unreasonable amount of time to consider the offer? Most offers and approvals should be good for at least 1 week before any secondary credit review would be needed.

- Style and Presentation. Listen to your business loan originator. Evaluate his speaking skills and see if his or her approach is educational, informative, consultive, and not aggressive or fast-talking. Does the originator listen and answer your questions fully? Does the originator use language like “guarantee”, and “no credit check”? If so, run the other way!

- Deceptive Marketing Practices. Are you receiving cold calls related to getting business loans? THIS IS A BIG RED FLAG! Never work with a lender or broker who would use this marking technique unless you have an existing relationship with them. Stay away from these boiler room tactics. Receiving offers in the mail can be an acceptable way for business lenders to market their services but beware of deceptive mail pieces that over-promise or use words like “guarantee”, “95% approval rate”, “no credit check”, “no paperwork needed” or over emphasize getting money fast.

Step 5: How to Get the Best Business Loan from Online Lenders: The Application Process

Once you have chosen your business loan originator and narrowed down what business finance products you want to apply for, it’s time to apply and get your offers. The business finance product selection and depending on the lender, the small business loan application, will dictate what documents are required. Ask your business loan originator what specifically will be needed for your small business loan application. It’s safe to say an application will need to be filled out and signed by all owners participating in the loan application.

Documents requested can range from a one-page application and bank statements to additional items like financial statements, proof of ownership of the business, personal identification, or other documentation to explain certain questions that may arise in the underwriting process depending on the lender.

Step 6: How to Choose the Best Option. Making the Right Decision

Ok, so you now have some offers. Remember a mail offer or other solicitation is not an offer. Always get a term sheet, commitment letter, or letter of intent and not just some quote in the body of an email when receiving offers from lenders. These documents will list all terms such as amount, term (length of repayment), rate, costs, payments, and any fees associated with the financing.

Does the offer fulfill the business needs and the best available for your business based on your qualifications? If so, then the only thing left to consider is whether you are comfortable with how the payments will impact your bottom line.

Take a moment to evaluate the cost versus benefit of getting financing for your business needs at this time. If you are nervous about the ability to repay or that it will negatively impact your business, then reconsider moving forward, but if you are comfortable with your answers to the above information, then accept and move forward with your business finance solution.

The Pros and Cons of Small Business Financing

Pros

- Can solve a problem with your business

- Can help make your business grow or expand and increase profits

- Can make the business easier to operate or improve efficiencies

- Can increase customer base with marketing or advertising

Cons

- Adds additional debt to the business balance sheet

- Payments that can impact expenses and cut into margins of profit

Frequently Asked Questions

Where Do I Find a Small Business Loan Originator?

It is not difficult to find or obtain business funding. A simple google search for “Business Loan Broker” or a specific product you are looking for like “small business loan”, “long-term business loan” will do the trick and provide many options. Another option is any recent mail offerings that you may have received and saved.

Should I Pay Any Fees Upfront Fees to a Small Business Loan Originator?

You DO NOT need to pay upfront fees to get most business loan products. Keep in mind, business funders and/or business lenders will charge fees that are deducted from proceeds at the time of funding. Always check the terms and conditions of all financing you are considering.

What Are Small Business Loan Rates in 2021?

The rates and origination fees can vary widely between business loan offers. The key is to shop and compare so you know you are getting a competitive offer.

Can I Qualify for a Small Business Loan If I Have Bad Credit? What kind of credit score do you need to get a business loan?

Yes, you can get approved for business funding if the business owner’s personal credit is considered bad credit. Be aware that your credit history will affect your options and what can be offered to you.

Can Small Business Owners Trust a Business Loan Lenders With Their Personal and Business Information?

If you do a proper check, then you have taken the necessary precautions to consider your data safe and secure. Remember there are no guarantees, so always use credit monitoring services and take the security steps to always protect your personal data and information.

The Bottom Line: Advice and Tips About Applying for a Business Loan for My Small Business

Whether it’s a Business Loan Broker, Direct Business Lender, or Business Finance Marketplace Platform, it’s important to ask questions and research the business loan originator you are choosing.

As a business owner, always ask yourself the key questions when getting a business loan for your business. What types of business financing products are offered? Does the Business Loan Originator have the experience and knowledge to assist me in finding the best product for my needs? Does the business loan originator not only have great customer service on the origination of my loan but also on the processing, funding, and servicing of my loan on the back end?

Always start by asking Why do I need the money? How am I going to put it to good use for the business? Have I been given all business financing options in the marketplace? Am I getting competitive rates, costs, and terms for my situation and credit profile? Have I done my cost verse benefit analysis for borrowing money for the business?

Always check your proposals and agreements for terms and conditions, including the cost of money (interest rate or factor rate), all closing or funding fees, term duration, payment frequency, personal or business guarantees, and any collateral requirements. If you ask the tough questions of yourself, you will be better armed to make great decisions.

How to Get a Business Loan Using Advancepoint Capital’s Marketplace

Applying for a loan with AdvancePoint Capital is as simple as 1, 2, 3. Let AdvancePoint Capital help you get the business finance option that fits your needs. Start with this online form, fill out the short application page, wait a few hours for your approval, and get your money!

The fast, convenient, and straightforward way to get approved and get the money you need for your business – now! Get your quote today by filling out our simple form.